Lesson 8: Reserves, Profit & APV

Back to Basic – Reserves

As discussed in Chapter 2, “increase in reserves” is an item in the revenue account that is unique to the insurance companies. Valuation actuary is responsible in determining appropriate level of reserves to be set aside for future liabilities, which are normally calculated using approaches stipulated in the guidelines issued by governments.

Back to Basic: Benefit Reserves Calculated using Net Premium

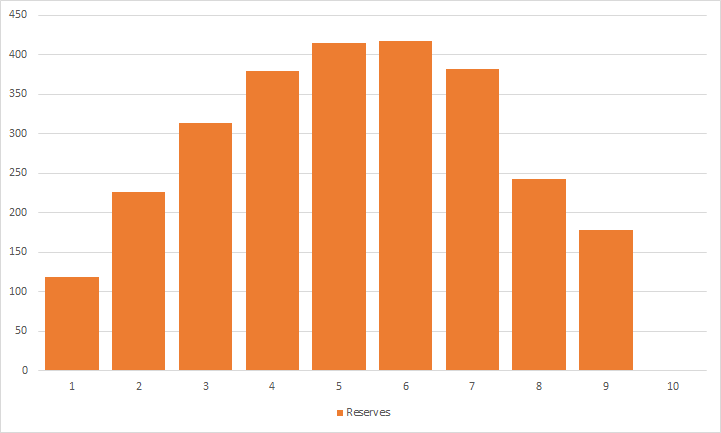

Why is setting reserves important to insurance business? Let’s take a 10-year regular premium term product below as an example (premiums and claims are projected on annual basis). As you seen from the chart below, which the premiums used are net benefit premiums:

- For policy year 1-5, the claim outgo is lower than the premiums paid. Hence, the excess and investment income arising shall be set aside as benefit reserves for future claims.

- For policy year 6-10, the claim outgo is higher than the premiums paid. Hence, when the premiums and investment income are insufficient to pay for the claim outgo, benefit reserves shall be released to cover the shortfall.

If you refer to the above chart for the movement of reserve balances:

- For policy year 1-5, we can observe increasing trend of reserve balance. However, the amount of increase reduces over time because the differences between premium and claim are getting smaller.

- For policy year 6, we can still observe a marginal increase in the reserve balance, as the is a slight excess after premium and investment income are used to pay for claim.

- For policy year 7-10, we can observe a reducing trend in reserve balance. This is because reserves are released to pay for the shortfalls due to higher claims. The reserve balance reduces to 0 at the end of policy year 10 as there is no more future liability (as the policy term is 10 years only).

Actuarial Valuation in Practice

In the past, valuation actuaries in Malaysia used net premium valuations in calculating statutory reserves, using prescribed assumptions (e.g. DGI96 mortality table, no lapse, fixed interest rate of 4% p.a.). The approach was consistent to the book value accounting adopted at that time.

When Malaysia moved to fair value accounting and Risk-based capital (“RBC”) framework, actuarial reserves are calculated using gross premium valuation, namely the actual premiums received from the policies. Different from net premium valuation, valuation actuaries need to consider all cash flows, including commissions and expenses that were omitted under net premium valuation, in setting up actuarial models used to calculate statutory reserves.

For valuation assumptions, RBC guidelines do not prescribe any specific assumptions, but to be determined by the valuation actuaries. However, to provide a comfortable cushion against the volatility in assumptions, valuation actuaries are required to set aside provisions for adverse deviations (“PRAD”) on top of the best estimate liabilities (which is normally known as reserves with 75% confidence interval).

- To derive reserves with PRAD, normally valuation actuaries apply assumptions that are more prudent than the best estimate assumptions. For example, valuation actuaries may increase mortality rates in order to produce higher reserves.

- Normally, the prudent assumptions are derived by apply a % to the best estimate assumptions, i.e. > 100% or < 100%.

- The selection of PRAD factors depends on the product features. For example, lapse supporting products may result in lower reserves when higher lapse assumptions are used.

Furthermore, PRAD also allows the surplus / profit to gradually emerge over the policy term, instead of being recognized immediately upon receipts of premiums (please note that gross premiums comprise many components, including profit margin). Under IFRS 17 framework, the contractual service margin (“CSM”) , which represents the unearned profits, will play a role in the emergence of profits over time.

Recent Development of Valuation Guidelines in Malaysia

Malaysian government has issued an exposure draft Valuation of Insurance and Takaful Liabilities on 24 December 2019, which is expected to replace the existing guidelines relating to actuarial valuation.