Lesson 4: Calculation B – Premium & Claims

Calculate Claims

Generally, claims can be projected using two approaches: (1) no. of terminates associated to death, TPD & CI; and (2) loss ratios.

Approach 1: Project Claims using No. of Terminations

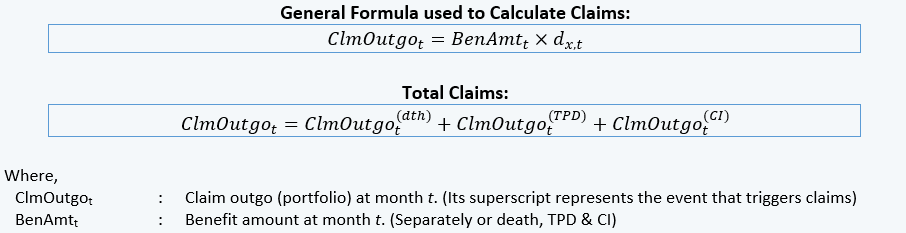

Normally, benefit amounts for death, TPD & CI are calculated separately. Apart from the coverage period (which TPD & CI coverage may cease earlier than death), sometimes different events may have different benefit amounts. For example, a product may pay funeral expense together with the current sum assured (Death Benefit = Current Sum Assured + Funereal Expense), which is only payable upon death.

Similarly, claims shall be calculated separate for each event before summing up as “total claims”:

Approach 2: Project Claims using Loss Ratio

Loss ratio method is normally used to project claims for medical insurance, personal accident and general insurance products, which premiums payable during a particular policy year are used to pay for the claims occur during the same policy year. This is different from products using level premiums, which involve savings in earlier policy years for higher incidences in later policy years.

Monthly claim outgo under loss ratio method is calculated using the following formula:

Setup the following fields in new columns under “calc_Portfolio” worksheet: (1) current sum assured; (2) benefit amounts for death, TPD & CI separately; (3) loss ratios (if applicable); and (2) claim outgo (total). “Current sum assured” field is required to allow for products with varying sum assured (which is derived from the “initial sum assured” entered in the “input” worksheet), such as mortgage reducing term assurance (“MRTA”).

Normally, we do not calculate “per policy” claim outgo or claim cost, unless we need to calculate asset share for the policy.